How Should Banks Choose Between WhatsApp vs SMS for Loan Reminders Safely?

Data from 100 million BFSI messages proves that the "WhatsApp vs SMS" debate misses the point. WhatsApp delivers 2.3x higher payment link engagement, but SMS remains essential for universal reach and compliance-critical alerts. The winning strategy is intelligent orchestration that routes messages through the optimal channel based on cost, deliverability, and customer preference. Thus, reducing total communication costs by 30-40% while improving collection performance.

Every month, Indian banks and NBFCs send millions of loan reminder messages. The question is no longer whether to use digital channels, but which deliver the best results while maintaining compliance and cost efficiency.

Data from over 100 million loan reminder messages across India's BFSI sector reveals: banks asking "WhatsApp or SMS?" are asking the wrong question. The competitive advantage comes from intelligent orchestration that leverages the best of both channels, strategically.

Why Do Most Banks Struggle With Loan Reminder Effectiveness?

Despite heavy investment in communication infrastructure, many banks experience poor collection rates, customer complaints about message overload, and vendor bills that don't align with actual delivery performance. The root cause is fragmentation.

When your SMS provider, WhatsApp Business API partner, email system, and in-app notification infrastructure operate in isolation, you lose visibility into what works and what doesn't. Different teams manage different channels, compliance requirements get interpreted inconsistently, and customers receive duplicate messages. This fragmentation means banks cannot measure true ROI across channels, cannot run systematic experiments to improve results, and remain exposed to regulatory risk from inconsistent compliance controls.

What Does Data From 100 Million Messages Reveal About Channel Performance?

SMS vs WhatsApp is not a choice. Orchestration makes both work better together.

Comparison of WhatsApp & SMS: Not Orchestrated vs Orchestrated

How Does WhatsApp Engagement Compare to SMS for Loan Collections?

WhatsApp Business API messages consistently deliver higher engagement for loan-related communications. Both channels achieve 90-98% open rates within 15 minutes. But the critical difference is action: customers are 2.3 times more likely to click payment links sent via WhatsApp than those sent through SMS.

The engagement advantage comes from WhatsApp's rich media capabilities. Whatsapp API has a robust system to validate business accounts and verified ticks that act as assurance for customers about security. On the other hand SMS with a URL in it are prone to suspicious activity, hence garners less trust and click throughs, for action.

A well-designed WhatsApp message includes the loan account number, outstanding amount, due date, and a direct payment button in a single readable format. SMS messages, constrained by 160-character limits and plain text, require customers to click through to external payment pages, to access complete details adding further friction that directly reduces collection performance.

What Are the Real Cost Differences Between WhatsApp and SMS?

Cost comparisons are more nuanced than just per-message pricing suggests. WhatsApp Business API pricing follows a conversation-based (customer initiated) model where banks pay for 24-hour windows (₹0.11 - .12 for utility messages), accommodating multiple messages per window. Transactional SMS typically costs ₹0.15 - 0.30 per message.

However, 3 hidden costs inflate SMS-only strategies:

Longer messages trigger multipart charges. A payment reminder with account details often exceeds 160 characters, resulting in 2-3 SMS charges per message.

Delivery rates for promotional content hover around 85-90%, meaning you pay for undelivered messages.

Manual vendor bill reconciliation consumes operational resources because invoices rarely match delivery logs.

Banks using intelligent orchestration platforms reduce overall communication costs by 30-40%, not through channel replacement but through optimisation. It automatically selects the most cost-effective channel, routes high-priority alerts through the most reliable path, and consolidates vendor billing into a single reconciled view.

When Does SMS Still Outperform WhatsApp in BFSI Communications?

SMS remains superior for specific use cases. Universal reach is its primary strength - every mobile customer receives SMS regardless of smartphone ownership, essential for rural and underbanked populations. OTP delivery requires predictable latency that SMS provides. It is more reliable than internet-dependent WhatsApp. Critical alerts like fraud notifications default to SMS to ensure receipt without data connectivity.

Optimal performance comes from intelligent routing, not channel exclusivity. Leading BFSI organizations use WhatsApp for engagement-driven communications while reserving SMS for compliance-critical alerts.

What Common Mistakes Do Banks Make When Choosing Between WhatsApp and SMS?

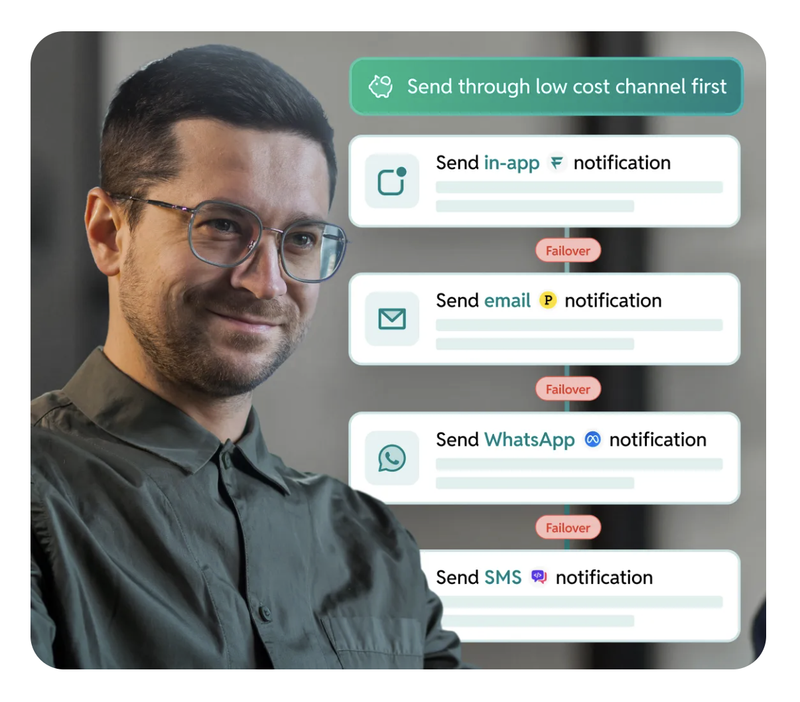

The binary "either-or" framing is the most expensive mistake. When banks treat channels as competitors, they negotiate separate vendor contracts with each requiring its own integration, compliance review, and invoice reconciliation. This prevents intelligent cost optimisation. For example, if WhatsApp delivery fails during peak hours, an orchestrated system routes the message through SMS failover automatically, while fragmented systems simply fail to complete the delivery.

Manual channel selection also creates compliance blind spots. Different teams apply their own interpretation of consent requirements across channels - creating regulatory exposure under DPDP Act and TRAI regulations. A customer who opts out of SMS marketing might continue receiving WhatsApp promotional messages because different systems manage different channels. Orchestration platforms maintain unified audit logs, eliminating these gaps.

How Does Intelligent Orchestration Solve the Channel Selection Problem?

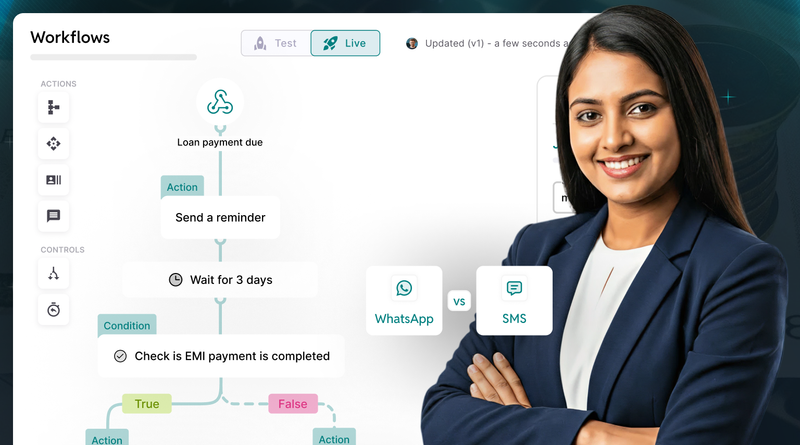

How Should Banks Design Multi-Channel Journey Flows?

Effective journey design treats communications as sequences, not isolated messages. A loan disbursement journey includes approval notification, document submission reminders, disbursement confirmation, and the first EMI reminder — each requiring channel selection based on priority, preference, and cost.

The journey begins with channel preference detection at loan application. Approval notifications use WhatsApp first for rich media, falling back to SMS within 60 seconds if delivery fails. Document submission reminders follow time-based escalation, for example: WhatsApp at 24 hours, WhatsApp plus email at 48 hours, adding SMS at 72 hours.

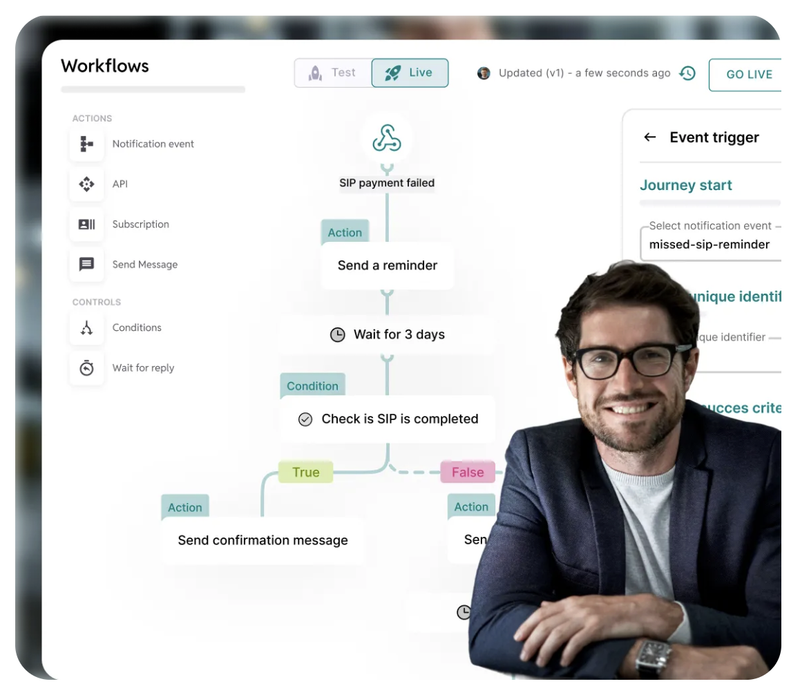

Platforms like Fyno allow banks to design these flows using visual no-code builders - defining channel priority, failover rules, and timing logic without engineering involvement. Leading NBFCs using Fyno Workflow builder for loan reminder journeys have noted improvement in document submission rates and reduction in loan processing time.

What Is Message Classification Optimisation and Why Does It Matter?

WhatsApp's conversation-based pricing creates optimisation opportunities most banks miss. Utility conversations open a 24-hour service window during which additional messages cost nothing. If a customer receives a disbursement confirmation (utility message) at 10 AM Monday, any follow-up before 10 AM Tuesday falls within the same window at zero incremental cost.

Consider a typical sequence: disbursement confirmation (Monday 10 AM), payment schedule reminder (Monday 6 PM), auto-debit setup prompt (Tuesday 8 AM). Without journey orchestration, each opens a new conversation leading to three separate charges. With intelligent routing, two messages fall within the initial window, reducing costs by 66%.

A mid-sized NBFC sending 500,000 loan messages monthly can reduce WhatsApp costs by ₹2-3 lakhs through classification optimisation alone. Additionally, TRAI's January 2026 directive mandated Pre-Tagging of Variables in SMS Content Templates and orchestration platforms like Fyno automate this across providers without manual vendor coordination.

How Can Systematic Experimentation Improve Collection Rates?

Banks can improve EMI collections by treating messaging as an experiment, not a fixed rule. Timing, message clarity, and channel order directly influence whether customers act.

Banks can run an experiment with delivery timing.

For example, testing morning versus evening EMI reminders to measure which time window leads to faster payments.

Another experiment is message structure.

Short reminders with a single payment action can be tested against longer explanations to see which drives higher completion.

Channel sequencing is the highest-impact test.

A bank can send WhatsApp first and trigger SMS only if the message is unread after a defined interval.

This approach can reduce costs without reducing collections. SMS acts as a fallback channel instead of a duplicate. But these experiments require unified orchestration. Without a single control layer, banks cannot test, measure, or optimize across SMS and WhatsApp together. Fyno enables these experiments safely at scale. It provides centralized routing, testing logic, and audit-ready tracking across both channels.

What Results Can Banks Expect From Communication Orchestration?

Karnataka Gramin Bank reduced OTP failure rates by 23% through intelligent multi-channel failover — when SMS OTP delivery fails in rural areas, the system sends via WhatsApp within 30 seconds.

Protium Finance improved EMI collection rates to 97% after implementing WhatsApp-first payment reminders with embedded UPI payment links.

Cost reduction comes from these and many other specific optimizations: automated vendor bill reconciliation (eliminating 8-15% invoice discrepancies), dynamic message formatting (reducing SMS costs by 12-18% by preventing multipart charges), intelligent channel routing (selecting lowest-cost effective path), and volume consolidation (unlocking better vendor pricing through unified orchestration).

For a mid-sized NBFC with a ₹500 crore loan portfolio, these improvements translate to ₹2-3 crore annual operational cost reduction and improved NPA ratios.

Why Does Communication Orchestration Matter for Digital Transformation?

Banks invest in core banking upgrades and mobile apps while managing communications through fragmented legacy systems. Intelligent orchestration serves as the nervous system connecting digital banking to customer touchpoints that can launch new strategies in hours rather than months.

When regulations change, business teams update compliance rules through no-code interfaces without engineering involvement. As DPDP Act, TRAI's template pre-tagging mandates, and RBI's digital lending guidelines intensify scrutiny, orchestration provides the centralized governance and consent management that manual approaches cannot match.

Banks treating communication infrastructure as strategic rather than operational unlock material advantages in customer experience, cost efficiency, and regulatory agility.

SUMMARY

Key Takeaways:

Cost optimization comes from intelligent orchestration - exploiting WhatsApp's 24-hour conversation windows (66% cost reduction per sequence), eliminating vendor overcharging (8-15% savings), and dynamic channel routing, not from channel replacement.

SMS remains essential for universal reach, compliance-critical OTP delivery, and offline-accessible fraud alerts.

Leading NBFCs report measurable results: 23% OTP failure reduction (Karnataka Gramin Bank), EMI collection improvement to 97% (Protium Finance)

TRAI's variable tagging mandate and DPDP Act requirements make centralized compliance governance increasingly critical. Orchestration platforms like Fyno automate template registration and consent management across providers.

Communication orchestration is a strategic digital transformation infrastructure enabling banks to launch new strategies in hours rather than months while maintaining unified regulatory compliance.