Compliant Customer Communications for Modern Banks: How Fyno Makes Regulation Effortless

TLDR: How Fyno enables compliant customer communications for banks

Compliant Customer Communications in banking means sending the right message through the right channel securely, with consent, and with proof. Fyno helps banks do this by unifying SMS, WhatsApp, email, and other channels under one API, with built-in consent management, audit logs, template controls, encryption, monitoring, and failover. That makes regulatory requirements easier to meet without constant custom engineering.

What “compliant customer communications” means in banking?

Compliant Customer Communications means every customer message is sent lawfully and safely: customers have opted in where required, sensitive data is protected, content follows messaging rules, delivery is traceable, and banks can produce audit evidence quickly. It’s not only about sending notifications, it’s about proving the bank followed the rules across every channel and touchpoint.

What regulatory requirements shape bank customer communication in India?

Banks in India operate under overlapping rules that govern where messages are routed, how customer data is collected and protected, what messaging content and opt-ins are allowed, and how cyber risk is monitored and reported. These requirements affect every customer touchpoint OTPs, transaction alerts, service updates, and marketing across SMS, WhatsApp, email, and more.

RBI localization requirements

RBI now requires banks to route customer communications through domestic channels rather than relying on international providers. In practice, this pushes banks to transition away from global communication platforms to local service providers without sacrificing delivery reliability, observability, or customer experience.

Many banks are actively reducing transactions via third-party CPaaS vendors and shifting towards direct integrations with telcos, as per RBI's recommendations. The operational burden is real: managing multiple telco integrations and ensuring real time compliance becomes a persistent challenge.

Data protection and privacy under DPDP 2023

The Digital Personal Data Protection Act (DPDP) 2023 establishes clear rules for handling customer data, including explicit consent requirements. Banks must obtain consent before collecting or using personal information, and that consent must be specific and easy to withdraw across every channel and use case.

The act also requires secure methods for storing and processing data, with the ability to detect and fix security breaches quickly. Banks must clearly explain why data is collected, how it will be used, and how long it will be retained.

TRAI guidelines for messaging

TRAI has specific rules for how banks send messages, especially around consent, traceability, and message suitability. Banks must only send messages to users who have explicitly opted in, maintain transparent audit trails with timestamps and delivery confirmations, and follow strict content regulations to ensure messages remain appropriate.

RBI cybersecurity framework

The RBI cybersecurity framework requires banks to maintain a dedicated cybersecurity policy separate from IT policies, designed to address cyber threats with precision. Banks must conduct continuous risk assessments, establish Security Operations Centers (SOCs) for real-time monitoring, and maintain robust incident response plans.

Board level oversight is essential, which makes cybersecurity not just a technical function but a core part of enterprise risk management.

What makes regulatory compliance hard for banks in day-to-day messaging?

Compliance becomes difficult when communications are spread across vendors, channels, and teams, each with different logs, controls, and workflows. Banks must prove what was sent, to whom, when, through which channel, and under what consent while also protecting data and adapting quickly as rules evolve.

Fragmented communication systems across channels and vendors

Most banks use multiple vendors for different channels SMS, WhatsApp, email, and more. This fragmentation makes it difficult to track compliance end-to-end, produce consistent reporting, or maintain a complete audit trail across every message type.

Many banks are implementing centralized systems for two reasons: to gain a unified view across multiple systems and to create comprehensive audit trails for compliance purposes.

Security and data protection at scale

Banks struggle to protect customer data while maintaining efficient communication. Implementing end-to-end encryption, secure data storage, and continuous monitoring across fragmented systems is complex, resource-intensive, and often duplicated across teams and vendors.

Adapting to changing regulations without slowing delivery

Regulations evolve rapidly, forcing banks to update processes and systems repeatedly. Without a flexible platform, even small updates can require significant time from IT teams slowing launches, increasing risk, and raising the cost of staying compliant.

Managing consent and preferences across teams

Banks must track customer consent across channels and ensure every message respects those preferences. This becomes harder when different teams manage different channels leading to gaps in visibility, inconsistent enforcement, and avoidable compliance exposure.

How does Fyno solve regulatory challenges in bank communication?

Fyno helps banks reduce compliance risk by centralizing customer communications across channels and embedding regulatory-ready capabilities into the platform. Instead of stitching together vendors and building compliance controls from scratch, banks can manage channels, consent, templates, audits, monitoring, and security in one operational layer.

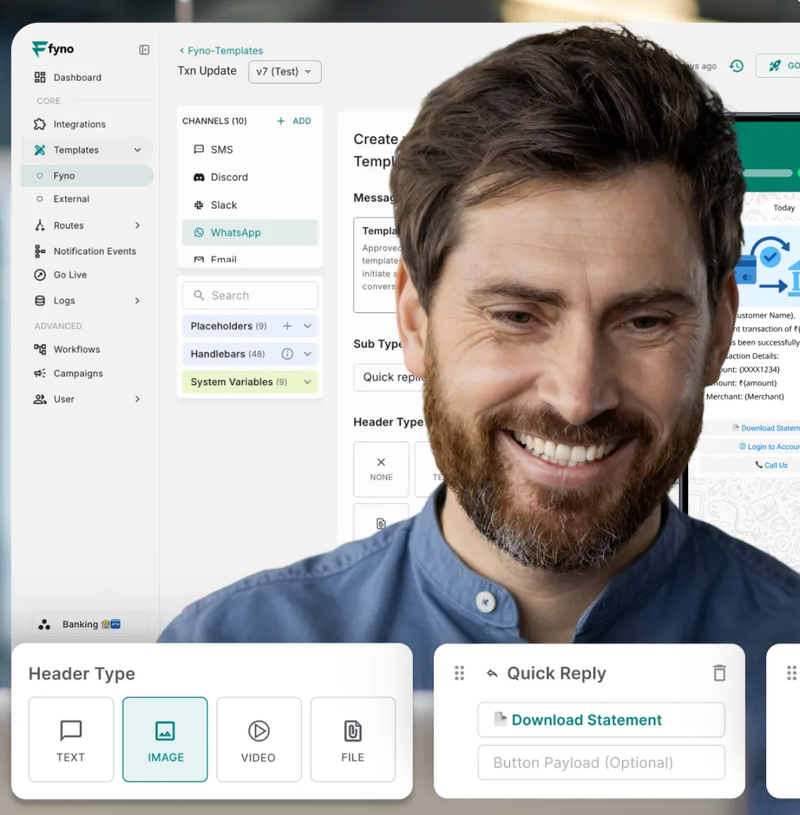

Unified API for all communication channels

Fyno provides a single API that connects with all communication channels, letting banks manage SMS, email, WhatsApp, and other channels from one platform. This centralized view makes it easier to monitor compliance, standardize controls, and generate reporting without reconciling fragmented vendor logs.

Built-in compliance features

Fyno includes native support for regulatory requirements like RBI localization, DPDP, and TRAI guidelines. Capabilities such as comprehensive audit logs, consent management, and data masking help banks maintain compliance without piling on additional development work for every change.

Centralized template management

Banks can create, store, and manage all message templates in one place, improving consistency across channels with the help of Fyno. The platform supports enforcement of regulatory requirements across different message types reducing the risk of non-compliant phrasing, missing disclaimers, or inconsistent formatting across teams.

Real-time monitoring and analytics

Fyno provides analytics on delivery, engagement, and compliance signals, so banks can identify issues early before they turn into regulatory concerns. This helps teams troubleshoot faster and demonstrate operational control when internal or external audits require evidence.

End-to-end encryption and data protection

Fyno includes security features such as end-to-end encryption, data masking, and secure storage to protect customer information in line with DPDP requirements. This supports safer handling of sensitive communication workflows without relying on ad-hoc controls across multiple vendors.

Automated failover mechanisms for critical messages

For high-criticality messages like OTPs and transaction alerts, Fyno supports intelligent failover that automatically switches channels if delivery fails. This improves reliability for time-sensitive notifications helping banks meet expectations around delivery assurance for important customer communications.

Regulatory mapping: requirements vs how Fyno helps

This quick mapping shows how banks can translate common regulatory expectations into operational controls, and where Fyno fits into that workflow.

What results can banks expect after implementing Fyno?

Banks using Fyno report improvements in compliance readiness and operational efficiency by reducing fragmentation and repeated engineering effort. In one example, one of the largest PSU banks in India reported saving 2–3 months of development effort and reducing engineering overhead by 80–90%, enabling teams to focus on core banking innovation instead of maintaining communication infrastructure.

This aligns with a broader pattern: consolidating channels, templates, consent, and audits into one system makes compliance easier to manage and easier to prove.

What’s next for regulatory compliance in banking communication?

As regulations keep evolving, banks need systems that can adapt quickly without frequent rebuilds. Fyno positions itself as that adaptable layer through continuous innovation, so banks can meet new requirements without major system overhauls.

The platform’s AI-driven features are described as helping banks anticipate regulatory needs and optimize communication strategies such as smart channel selection and dynamic budget optimization supporting both compliance and customer experience in a rapidly changing landscape.

Based on our conversations with over 30 banks, we've identified the key regulatory challenges in customer communication and how Fyno's platform addresses them.

Getting started: a practical rollout checklist for banks

A compliant rollout is less about “adding one more vendor” and more about standardizing controls across channels.

Inventory your channels and vendors: SMS, WhatsApp, email, and any internal tools.

Define message categories: OTPs, transaction alerts, service updates, marketing, collections, etc.

Standardize templates centrally: move channel-specific templates into one governed library.

Implement consent + preference rules: align opt-ins and withdrawal paths across channels.

Turn on audit trails by default: ensure timestamps and delivery confirmations are retained.

Apply data protection controls: masking, encryption, secure storage for sensitive fields.

Set monitoring + escalation: define what constitutes a compliance issue and who owns response.

Validate failover for critical messages: test OTP/alerts delivery behavior under failure conditions.

SUMMARY

Compliant Customer Communications in banking depends on consistent consent enforcement, secure handling of customer data, clear audit trails, and reliable delivery across every channel. When SMS, WhatsApp, and email are managed through fragmented vendors and teams, compliance becomes harder to enforce and even harder to prove during audits. By centralizing channels under a unified API and adding built-in controls like consent management, governed templates, audit logs, encryption, monitoring, and intelligent failover, Fyno helps banks reduce regulatory risk, adapt faster to changing requirements, and maintain a strong customer experience without excessive engineering overhead.

Comments

Your comment has been submitted